Noah's Arc 2024 Q2 Newsletter

The American Workforce & Energy Demand

Executive Summary

American Workforce: A Tale Of Two Groups

Stagflation Update: My earlier concerns about stagflation are now likely overblown as inflation stabilizes and economic growth slows. Goods inflation remains a risk due to potential supply chain disruptions, while services inflation is harder to control.

Workforce Trends: The US citizen workforce has plateaued, with many retiring due to strong market valuations. Workforce growth is now primarily driven by non-US citizens, impacting small businesses that struggle to sponsor non-citizen employment.

Energy: Wealthy Nations Use More Of It

Power Demand: The US power grid faces increased demand from EV adoption and AI technology, but it is under-prepared. Companies like Primoris (a construction company) & NRG Energy in unregulated markets could benefit from strong pricing power due to fixed supply and rising demand.

Personal Note: A Focus On Process

Research and Writing: Writing and actually publishing my investment ideas have significantly improved my decision-making. To all of those who keep reading this quarterly letter (or if you read my investment ideas), thank you.

American Workforce

Last quarter, I wrote about how stagflation (persistently higher than desired inflation + anemic economic growth) is a real risk to the US economy. While I believe we are starting to see the economy slow based on multiple economic indicators that came out with the May data, inflation is running basically flat now month-over month.

I’ll call a spade a spade. While some analysts now believe there is a risk of stagflation, I believe now my personal concerns of stagflation (for now) were probably wrong.

Inflation is now moving lower (while the underlying economy slows as well). Goods prices are now decreasing as consumers are pushing back. Goods prices could snap back, however, in the event of another supply chain disruption but the odds of this are unknown. Goods have the same commodity price risks that I mentioned in my last newsletter and in a newsletter back in 2022. For now, they are subdued. This is hard to predict going forward.

Services prices are harder to put a lid on. This is one of the parts of inflation that has been hard to beat. A key piece of deciding inflation (in the long term) is going to be services inflation. Service inflation is directly correlated with the amount of people in the US that are able to work (and at what price).

Over the last 3 months I have been looking at population data. What's interesting is that the American workforce is a tale of two labor groups:

US Citizens: Workforce population has plateaued. The number of Americans actually employed has declined by some estimates, reflecting more Americans retiring due to strong start market valuations and equity in their homes meaning they do not have to work as long

Non-US Citizens: This group is responsible for nearly all of the growth in the US workforce since COVID.

While the US has always been a nation of immigrants, what's notable here is that the core US citizen labor force is no longer growing (it usually has grown in the past in tandem with the foreign born workforce). This has massive implications for services businesses that have to rely on labor in the US to run their business. Many small businesses (however) struggle to sponsor non-citizen employment. It means for many small businesses, this is why labor has been hard to find even as the economy has cooled and why many businesses choose to cut employment hours vs. fire employees all together. It's also why services inflation may stay higher for longer, while goods inflation moves down to help overall inflation become more reasonable.

It’s a delicate relationship (as I mentioned above). Goods inflation could move up quickly and unexpectedly.

My big point on population has to do with consumption. In essence, in the super long run, some goods growth will be subdued (consumers can only consume so much stuff physically). Services may be a different story. Specifically, utilities and power are the part that I like the most.

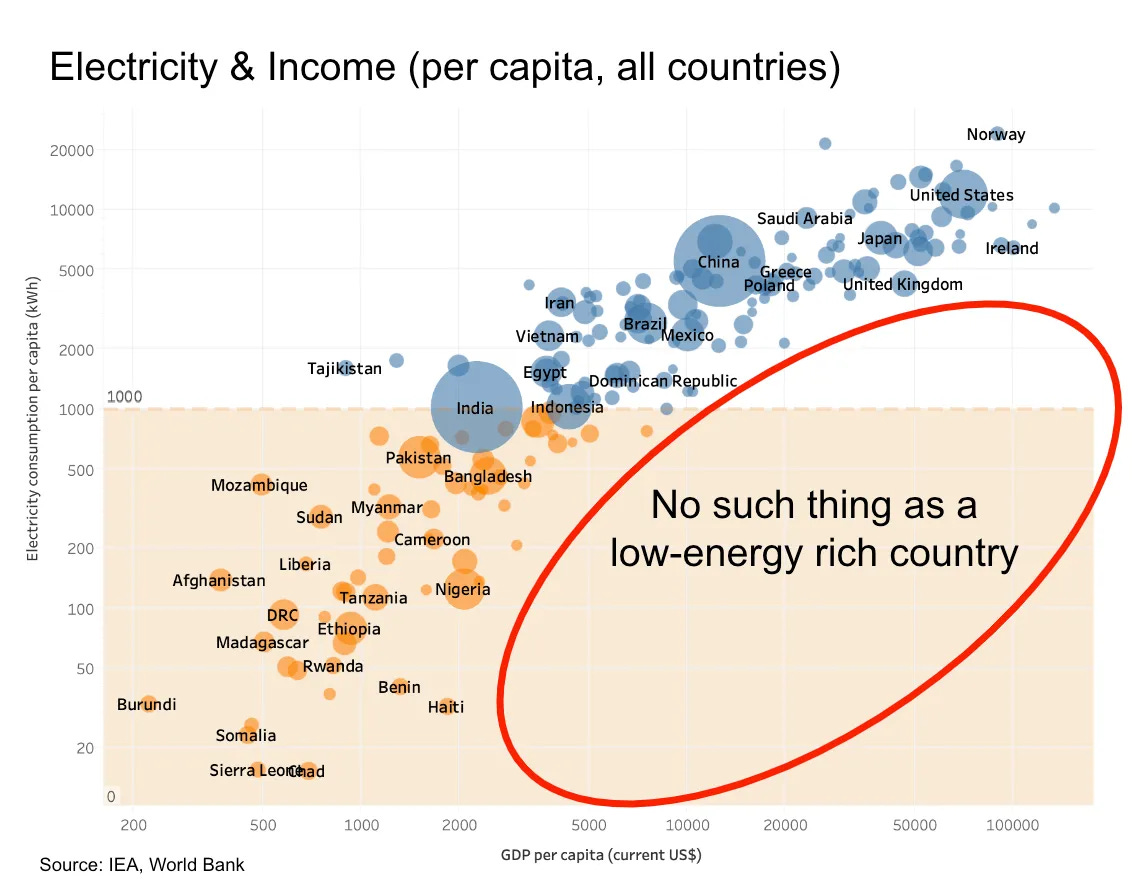

Energy: Wealthy Nations Use More Of It

While the US native born working population is plateauing (approx. 100% of the growth over the last 4-5 years since COVID has been from an increase in non-US citizen employment), power demand per capita (both US citizens and US residents) is likely to reaccelerate higher as more American buy EVs, and leverage power-intensive AI technology in our lives.

However, the US power grid (besides being woefully underprepared for cyber attacks) is likely under-built with these new influxes of demand. Power companies in unregulated markets (like Texas) will likely have strong pricing power as demand goes up but supply is relatively fixed (you can’t build a power plant overnight). The grid in Texas is already strained from the record demand, and power operators there like NRG Energy, have experienced largely stronger profits.

If you have a Seeking Alpha subscription, I’ve been writing on the platform to help keep a record of my ideas (and their subsequent performance) now for about 9 months. You can check it out here if you’re curious. It’s cool that a couple thousand people now have decided my content is interesting enough to follow me.

Of the 127 research pieces I’ve written over the last 9 months, Primoris has been one my favorite ideas.

Primoris is a construction and utility maintenance company that operates primarily in the Sunbelt of the US (but also has some operations back here in Michigan).

Due to the explosion of power demand in parts of the US, the company has seen their order-book jump and revenue growth has been strong. In essence, the company has been riding the same trends that have powered some of the best performing stocks over the last 12 months (AI).

Yet, also at the same time, since wealthy nations tend to use more energy resources per capita and also tend to be more productive (per capita), the company will do well regardless if the population in the US continues to grow (or plateau).

It's a fascinating set up (in my opinion).

Shares have run up a lot since I first wrote about them in October so I would not be surprised if there was a pull back. But I am long run bullish.

These investment stories are the core of what Noah’s Arc is about. Investing in companies (and industries) undergoing a 21st century transformation and are set to see their respective equities re-rate higher as the market appreciates their new business model and opportunities.

Personal Note: A Focus On Process

I’ve spent a lot of time this year trying to focus on how I can get more high quality investment ideas in-front of me so I can make better decisions. Writing more has helped a lot, and something that I wish I had personally done way earlier.

Better late than never. The now 127 published investment ideas I’ve written (and the 6-7 more I have in the process of drafting) have helped me drop earlier investment ideas that I should have dropped sooner, while also finding more investment ideas so I know there is always an alternative.

It’s so much easier to compare a bad investment idea to a good one when you have more good ones to evaluate with.

I’m of course no Warren Buffett, but I’m learning a ton. To the investors in Noah’s Arc Capital Partners who read this newsletter (and to everyone else who has decided to keep this newsletter in their inbox after over 3 years now): thank you. Writing (including this newsletter) is helping grow this business, and helping grow me as a person.

Till next quarter,

Noah