Noahs' Arc 2023 Q3 Newsletter

The changing world of Private Equity and Interest Rates

Welcome to Noahs’ Arc Q3 2023 Newsletter. We’re talking about the changing world of Private Equity and Interest rates. While some of our views may appear short run pessimistic , we think there’re still plenty of reasons to remain bullish on select aspects of the market.

No aspect of this material is intended to provide, or should be construed as providing, any investment, tax or other financial related advice of any kind. You should not consider any content herein or any subsequent services provided to be a substitute for professional financial advice. If you choose to engage in transactions based on the content herein, then such decision and transactions and any consequences flowing therefrom are your sole responsibility. Noahs’ Arc does not provide tailored investment advice to any person directly, indirectly, implicitly, or in any manner whatsoever.

Executive Summary:

Private Equity with Private Troubles?: We examine how Private Equity, one of the most popular asset classes among wealthy investors, is undergoing immense change with sustained higher interest rates and new SEC regulations.

US Debt–Adding New Supply: As inflation continues to decline and the Federal Reserve nears the peak of its rate cycle, we examine how increasing US funding needs will change what the neutral “real” interest rate is in the US and what its impacts might be.

Personal Note: Noah and I are back in Ann Arbor for another year! While school is done for Cox (and almost for Jacobs), we talk about what’s next for us.

Private Equity with Private Troubles?

Private Equity rose to prominence in the 1980s with the decline in the Federal Reserve's interest rates as the runaway inflation from the 1970s abated, and firms like Kohlberg, Kravis, & Roberts (KKR) rose to prominence.

For those who are not familiar, Private Equity firms typically operate under the following structure:

PE fund managers (General Partners) identify industries in which private companies could see accelerated growth, given restructuring and new management

PE funds raise equity capital from investors

PE funds select a company to purchase, called a portfolio company after acquisition

PE funds typically borrow against the portfolio company’s future cash flow to raise most of the capital to fund the buyout (these are called leverage buyouts/LBOs)

PE funds implement changes to grow the company, raise profitability, pay down the debt, and then sell the portfolio company to a new firm or take it public

With declining interest rates since the 1980s to 2020, this worked great. While PE firms were tasked with growing the portfolio companies, the single biggest driver of returns appears to be (on average) declining interest rates. As rates fell, PE funds could refinance the debt to lower interest rate costs (increase net income) and also decrease the discount rate these firms were valued with, therefore increasing the present value of the firm.

In fact, studies show that much of the alpha this industry generated over public markets and hedge funds in the years since 2008 was accomplished simply because the returns were leveraged.

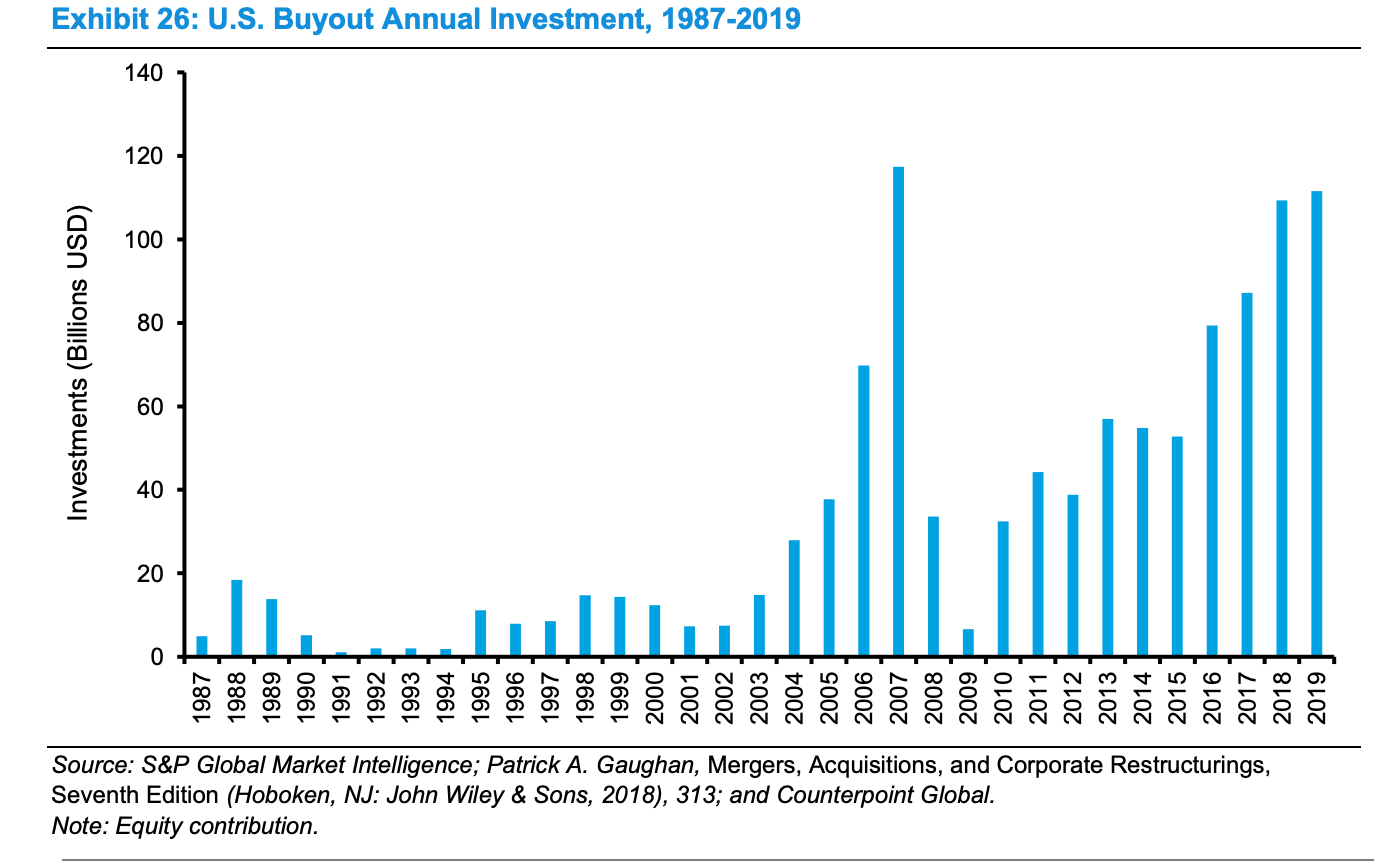

Even though PE as an asset class has been very attractive, (see the graph below), studies have shown that if an investor used margin to purchase an equivalent basket of public securities, they would have achieved similar or better returns as compared to investing in a private equity fund.

Source:

The beauty lay in the declining interest rates, which was a massive tailwind for PE managers.

However, since the Fed began tightening monetary policy to curb inflationary pressures in 2022, the climate of perpetually declining interest rates hit a rough patch; we argue below that this may continue.

This transition has posed a challenge for the PE industry, which has historically been accustomed to the tailwinds provided by falling interest rates. It’s changed the game for Hedge Funds, too, which have historically been structured to cherry-pick publicly traded winners and losers, thus often performing better in higher interest rate environments where the gap between the good companies and the poor ones widens.

In the Private Equity world, higher interest rates have impacted some investments by exponentially increasing the interest rate bill, resulting in an increase in PIK (Payment In Kind) interest payments by PE fund managers to creditors.

During this period, more hedge funds outperformed public market passive strategies, highlighting the shift in the tide.

Interestingly, despite the interest rate uptick, the often leveraged private equity funds have managed to hold their ground reasonably well when compared to public stocks. However, this resilience may have more to do with how the fund is structured vs. how the underlying portfolio companies are actually doing.

Private funds that invest in private assets (not stocks or bonds) are structured to eventually sunset and liquidate. The year these vehicles launch is called their vintage (think wine); unlike a good merlot, though, they usually have a lifespan of 7-10 years. This means the fund manager has to buy/invest in the portfolio company, improve its value, and then sell it within the window that the investors signed up for.

When PE funds and their managers do not achieve the targeted returns within the initial fund window, they can choose to extend the length of the fund by a couple of years to buy more time, bringing the length closer to 10 years than 7..,

What we were seeing is the average age of funds going up and the average vintage year getting older. With a lot of PE money chasing private businesses, it's inevitable that many of these managers did not get a steller deal and needed to extend the fund in hopes of the valuation eventually rising enough to hit their target return.

This creates more problems than it solves: PE funds are increasingly going back to their investors asking for more cash to fund new funds. This suggests that on average, PE funds were soliciting more fresh capital from their LP investors each quarter than what was being returned in distributions as funds extend their lives. PE funds are turning to negative cash flow vehicles for some investors.

The timing of cash flows is proving tough for some pension funds, some of which are looking to cap or reduce their PE investment allocations due to the changing cash flow nature of the asset and longer cycles. Of course, the very reason pension funds are moving away from PE funds is because of the PE funds’ new penchant for retaining investments for longer while soliciting more funds to cushion their higher interest obligations. It creates a vicious cycle.

Now, the Securities and Exchange Commission (SEC) has added another complexity by introducing new rules on how private funds value their assets. If these rules, currently undergoing litigation, are adopted and enforced, the level of discretion that PE, REPE (Real Estate Private Equity), and VC funds have over asset valuations is set to diminish.

The implications could be substantial if they hold ground. On the one hand, they could bring a new era of transparency for LP investors, more disclosures over side letters, special fee breaks, and more rigorous valuation estimates. On the other hand, as Buffett has said: “Only when the tide goes out do you learn who has been swimming naked.”

We’re not saying all PE funds are improperly valuing their assets… we’re simply noting that the incentives exist for them to be generous in their asset valuation marks.

The charm of private funds has always been their steady growth narrative. The big question now is, how much of this narrative was actually rooted in reality?

The US Debt Conundrum:

As inflation trends downwards and the Federal Reserve likely nearing its rate cycle peak, the focus shifts towards the growing US funding needs.

The US continues to borrow extensively, issuing approximately $5.1 billion worth of debt daily.

The interest payments alone are expected to surpass $1 trillion the next two fiscal years. Presently, the average interest rate on US debt hovers around 2.7%. However, with 40% of the US debt being refinanced annually due to short-term financing, the rate might edge towards the 4-5% range as indicated by the current curve. This change could have significant implications, particularly if the deficit to GDP ratio (negative) surpasses the nominal GDP growth (real GDP growth + inflation rate).

There's an argument to be made that even if the Federal Reserve decides to lower interest rates, the long-term interest rates might stay elevated due to the US government's continuous funding needs as entitlements such as social security creep up, and the average interest rate on the debt rises.

This scenario exemplifies a typical supply side crowding out, just like in econ class in college. Government debt supplies exceeding demand typically keeps long-term rates high. This could impact long-dated assets, both private and public, in a notable manner.

Despite this, we remain steady on our investment thesis. We maintain our belief in investing in 20th-century companies transitioning into the 21st-century realm, and believe that there continue to be incredible opportunities.

As market dynamics alter, we anticipate the market to favor high-quality companies even more, ones that are valued on the profits they make today vs. often intangible hopes of tomorrow.

Personal Note:

Noah and I are back in Ann Arbor for another year! Jacobs is finishing up some classes for his math minor as we both pursue this business full time.

One thing that has stuck with both of us the last couple of months is a focus on processes in our business, even if it's modestly sized. Nothing scales if it cannot be repeated over and over. This comes from process. While we’ve talked about Ultima Insights in the past: we’re treating it as a refinement of process.

Any hedge fund is only as good as its insights. While we remain confident that Noahs’ Arc can (and has) produced high quality investment ideas, we know with Ultima we can do even better. Our own skills are what allows our fund to operate today. Ultima is what will allow us to create an even more interesting strategy tomorrow.

Creating a hedge fund when you’re in your early 20s is not supposed to happen… it's not supposed to work.

In the long run, that’s why we need to be different. Our processes have to be unique.

As always, we appreciate you taking the time to read our notes.

Till next time,

-Noah & Noah