Noahs' Arc 2022 Q1 Newsletter

Ukraine, Passive Investing, Subtractive Thinking

Welcome to Noahs’ Arc’s first newsletter of the year. Comments on Ukraine, passive investing, subtractive thinking, and the fund itself below.

No aspect of this material is intended to provide, or should be construed as providing, any investment, tax or other financial related advice of any kind. You should not consider any content herein or any subsequent services provided to be a substitute for professional financial advice. If you choose to engage in transactions based on the content herein, then such decision and transactions and any consequences flowing therefrom are your sole responsibility. Noahs’ Arc does not provide tailored investment advice to any person directly, indirectly, implicitly, or in any manner whatsoever.

Executive Summary

The Ukraine and De-Globalization - We are viewing the conflict in the Ukraine as a symptom of and move towards De-Globalization.

The Waning of Passive Investing - A discussion on the rising risks of passive investing centered on the buoying of indices by globally dependent tech names.

Subtractive Investing - We articulate a useful way to think about screening; even if filters may cause us to miss winners, they can certainly help us to avoid losers.

Recap of our Winter, Going Forward - We’re officially launching our fund in April and are heading to the Berkshire Hathaway meeting in a month!

The Ukraine and De-Globalization

While our strategy doesn’t bet on quick trades or specific global events, we’d be remiss to not mention the elephant in the room: the Ukraine.

As is always the case with geopolitical instability, the events in Europe are perpetuating the uncertainty that has rocked the markets since the beginning of COVID. We’re not military strategists, so we’re not here to comment on the status of something fluid and unfamiliar to us. (That being said, we have linked an intriguing piece of journalism about the conflict here).

One thing we will note is the way that this war is in line with the De-Globalization that was started with COVID-19. While COVID pushed nations into their bunkers, this conflict is pushing nations to stick the barrels of guns out of the windows of those very bunkers. It is a hard pill to swallow, but the message is clear: violent, kinetic warfare is still possible, even in a globalized society and in a place very close to home for many.

Further, the turmoil stands to reiterate the supply chain fragility exposed by COVID-19 in a completely new way - clearly, our access to natural resources is not only susceptible to acts of god, but also to acts of man.

Increasing global disruptions have a secondary effect: we believe that much of the foundation that supports the modern index-passive investing mandate is rooted in globalization, a potentially declining trend. Passive investing tends to work best when global participants are pushing for stability and when the rule of law reigns.

The Waning of Passive Investing

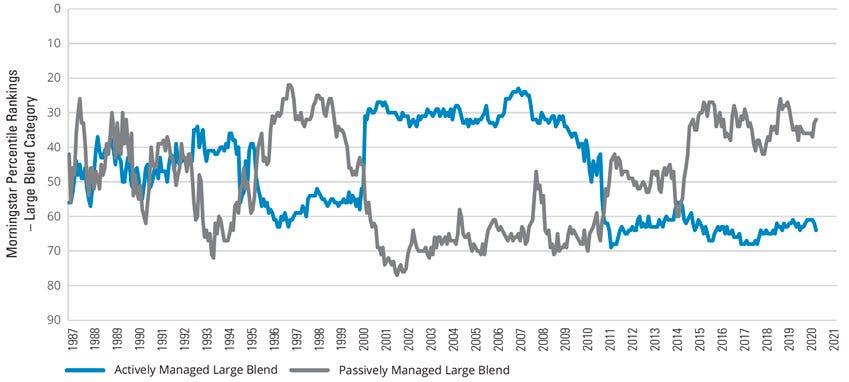

Passive investing has the huge driver of investor returns in most portfolios for the better part of 20 years. The simple strategy of buying a fund that tracks a major index (like the S&P 500 or the NASDAQ) has proven to be low costs and incredibly lucrative. However, like sectors or consumer purchasing trends, even passive investing can fade in and out.

The graph below shows a performance score MorningStar has given to a collection of passive funds and active funds over the course of over 3 decades.

In addition, we’ll link here how the two investment styles have compared year to year since 1990. In the bigger picture, it's pretty close (contrary to current market sentiment). 14 out of the last 32 years go to active investing, 17 years to passive, and 2010 was a tie. What's notable is that these years of beating or lagging each other tend to be path dependent, meaning that one year of active strategies doing well is generally preceded by more, such as between 2000 and 2009.

With the general gentle melt upward since 2008 (barring COVID, of course), we’ve seen the power of putting aside money in an index fund and letting it sit. However, one possible key underpinning of this has been global stability.

If we look at the returns of major global indices (China, Europe, etc), most have performed mediocre since 2009. The winner of this assessment has been the US market, pushed forwards by increased valuations in global tech firms and global brands.

In the wake of 2008, US companies were able to use cheap credit, strong innovation, and stable branding to gain share in key markets. US banks dominate global financing, Amazon is the largest E-Commerce firm in Europe, and AWS or Microsoft’s Azure power most global IT cloud infrastructure systems. While foreign revenues of S&P 500 companies have only risen by about 5% over the last decade, this has been driven by an increased share on the part of tech companies and an accompanying decline for natural resource companies; in other words, the aggregate growth in foreign revenues for tech companies is larger than 5%. As one example of large exposures, FactSet estimates that Microsoft gets more than 50% of its revenue from outside the states, with more than 10% coming from China. As global stability is questioned, there is a strong potential for higher costs, market share fragmentation, and, resultantly, lower profits.

What’s even more concerning than where these US based companies are getting their revenue from is where their supply chains are located… As one very poignant example, it is no secret that around 60% of semiconductors come from Taiwan. Tracking it back further, about 50% of the world’s neon needed for chip production comes from the Ukraine.

Tech is fueled by semiconductors, and US indices are fueled by tech. Afterall, over 40% of the S&P 500’s value is composed of tech companies.

While it might be easy to say “I own the S&P 500, so I have broad diversification and exposure,” the reality is that you likely do not. The top 5 companies in the S&P 500 represent 16% of the index’s value. The top 50 companies represent 50% of the index’s value. Many of these firms are large, global, tech companies. The results are stark: a bet on the S&P 500 right now is a bet on tech, and a bet on tech may be largely dependent on global stability and working supply chains. And as this WSJ documentary keenly shows/illustrates for us, the prospect that global stability and working supply chains will always be there for us in the future is not certain.

With over $11 Trillion in assets pegged to passive funds, many of which simply mirror the S&P 500 or the NASDAQ, in the event of disruptions, money could stampede out the same doors it's been continuously flowing into since 2009.

With this problem in mind, we have personally elected to employ subtractive filters to completely avoid some of the more volatile investments the market has to offer.

Subtractive Investing

To reiterate, we do not think that passive investing is a “bad” idea, so to speak; rather, we are uncomfortable with some of the risks that we would implicitly assume if we were simply indexing. A solution to this is knowing many of the risks one should or wants to avoid; doing so can greatly reduce your search pool in a very productive and effective way. Nassim Nicholas Taleb treats this subject expertly in Antifragile, denoted as “Via Negativa,” but we take our stab at it here.

A simple example may be refusing to purchase companies that have yet to turn a profit. While this may remove many market changing growth stories from our search pool, it also unilaterally eliminates countless penny stocks, over hyped and overvalued tech plays, and many otherwise speculative companies.

More than just swiping aside entire sectors, this sort of metric can also hone our search in the sectors we do decide to move forward with. In mining, it prevents us from committing cash to exploratory mines and junior mining operations struggling to get off the ground.

This is only one example of a rule with which one can subtract. It is not a condemnation of companies that have yet to bring in a profit, nor is it an expression of the belief that one cannot post returns investing in them. Rather, it is a useful way to get closer to a pool of companies that we believe are robust and play well with our strategy.

A Pleasant Side Effect: The Information Edge

Seeing as our subtractive search criteria often leave us with the not so glamorous companies, (the unexciting ones that don’t tend to 3x in value) these sectors not only typically see less investment, but there’s also less coverage on the names. For whatever reason, whether it be a human bias towards the volatile or simply that most people find mines and agriculture companies boring, the knowledge barrier needed to achieve an actionable information edge is much less rigorous than if one finds themselves competing with the hordes of investors chasing alpha in and around tech.

However, this information edge just happens to be working in our favor as of now - since it is not necessarily a search criteria, it may not be a permanent advantage of our strategy.

Full Circle

With subtractive search criteria, which is by no means our original thought, merely a useful way to understand screening, we have ended up with many companies that stand to resist some of the dangers of a more volatile world, and, in some cases, even benefit from that volatile world.

Recap of Winter and looking into the Spring

Despite the spotty weather making us yearn for the sun and cherish each bright day, the last few months have been quite productive and fun… after all, everything is now in place for our Partnership to launch in April! A big thanks to anyone and everyone who has helped us in any way at all.

Otherwise, we’ve continued to meet fascinating people from whom we’ve heard exceptional, intriguing stories that have enriched our minds.

Our fun will continue at the end of next month when we make the sacred pilgrimage to Omaha for the Berkshire Hathaway annual shareholders meeting…. It will be an honor and a privilege to be in the same room as Warren Buffett and Charlie Munger.

Thanks again for your support, and, as always, we appreciate the feedback! Enjoy the Michigan spring, full of its frigid April mornings and sweltering March afternoons.

Best,

Noah & Noah

No aspect of this material is intended to provide, or should be construed as providing, any investment, tax or other financial related advice of any kind. You should not consider any content herein or any subsequent services provided to be a substitute for professional financial advice. If you choose to engage in transactions based on the content herein, then such decision and transactions and any consequences flowing therefrom are your sole responsibility. Noahs’ Arc does not provide tailored investment advice to any person directly, indirectly, implicitly, or in any manner whatsoever.