Noah + Noah 2021 Q1 Outlook

Welcome to the starting line...

Hi all!

We are thrilled to finally be sending out our first quarterly update on our collective journey to start our small private fund. If you don’t know us, our names are Noah Cox and Noah Jacobs, and we hope that by our graduation from the University of Michigan Ross School of Business in May 2023, we will have made a viable career out of this investing venture.

The goal of this first newsletter is to give you an idea of not only how we think about the financial markets, but also about how we act on those thoughts. Here is an outline:

Fund Strategy

Macro Trends

Fund Performance

Attached, you’ll also find equity research reports for Hawaiian Holdings and Bank of New York Mellon, two names that we’ve traded on for the last 6 months or so.

We would greatly appreciate you sharing our updates with anyone who you think might find them interesting or who would otherwise have feedback for us. Additionally, if you yourself have any questions or thoughts on the work we outline here, feel free to shoot us an email or a text; some of our contact info is at the bottom of this post.

If you were forwarded this email, you can sign up to be notified directly about our next update by clicking “Subscribe Now” directly below.

Of course, all thoughts contained within this email are NOT investment advice; we are NOT registered as investment advisors or investment advisor representatives. Everything included is simply our own research; there are no recommendations being made.

Fund Strategy

In the future, we will be releasing both a pitch deck and thorough Investment Thesis Report on our strategy. In the meantime, we’ve decided to outline it in broad strokes below; along the way, we illustrate the strategy with our implementation in the airline sector.

Before we get started, one question we’re constantly asked is why we don’t just buy shares. For you math whizzes out there, we subscribe to the belief that stock returns are log normally rather than normally distributed. In layman’s terms, high impact negative events are more common than most financial models price in. While we’ll thoroughly unpack that statement in later posts, the general idea is that by implementing our strategy rather than buying stock, we are trying to prepare ourselves for negative price action while still keeping cash flow positive, even in sideways markets.

Pick a Sector

Pick Stocks

Sell Cash Secured Puts

Buy Insurance

Repeat or Sell Covered Calls

1) Pick a Sector

We start by researching the macroeconomic pros and cons of a sector; we will discuss what we’re finding with each other and see if it is an appropriate fit that is exposed to positive tailwinds. Our four picks so far have been semiconductors, airlines, banks, and construction (although this started as utilities). Each sector has received an approx. 25% portfolio allocation.

We began discussing airlines in depth in July. For us, the rationale was undoubtedly in line with other investors - we thought that the industry already enjoyed tame valuations prior to the pandemic, so of course the fire sale that COVID provided presented a number of tempting offers.

2) Pick Stocks

Next, we screen companies within the sector. Some things we look at are cash positions, debt, cash flow, PP&E, and trends in revenue and net income. Of course, the sector we’re watching will influence some of what we’re on the lookout for: while a high book value for airline stocks is desirable for a recovery play, net income growth in the names could not be expected between 2019 and 2020.

If we struggle to find good picks this way, we’ll go up or downstream from major players in the industry. For instance, we found Amkor, a chip tester, by looking at the supply chain of large chipmakers, and Primoris Services Corp, a construction company contracted with major utilities, by looking at the supply chain of major utility companies.

As the numbers begin to check the appropriate boxes, we start asking deeper questions about the business to make sure that we understand what the company is doing and if it fits into the sector’s story. For airlines in particular, a caveat in the recovery tale was a quicker rebound for domestic leisure travel, seeing as business travel is threatened by a potential permanent impairment and international borders are generally more difficult to open.

All things considered, the airlines we settled on were Hawaiian Holdings, Spirit Airlines, and Southwest Airlines. All of these players have strong domestic footprints and focus on leisure travel more so than business. Again, our Hawaiian research is at the bottom of this letter.

3) Sell Cash Secured Puts

With the sector and stocks selected, everything is in place to implement the strategy by selling cash secured puts on the selected stocks. A cash secured put is a promise to buy 100 shares at a predetermined price. In exchange for the promise, the put seller is given cash.

By selling puts rather than purchasing shares directly, we can commit to a price below the current cost of the shares on the open market while getting paid to do so. This helps to insulate us from short term, minor market fluctuations; unless our put is “exercised” and we have to buy shares, the stock moving a little lower has no impact on our portfolio. We’d like to emphasize the fact that we DO NOT use margin. For every put we sell, we have the cash set aside to buy shares.

4) Buy Insurance

Even though we hope that we’ve chosen good stocks, we know that the market may disagree with us, and we can even be flat out wrong. So, we look for protection against more substantial moves in each sector by purchasing puts on ETFs tracking the space to bet against ourselves.

By purchasing puts, we receive positive returns when the sector drops significantly, mitigating some of our losses. To get an idea of just how much coverage we can buy, we use a calculator that compares an estimation of the return on purchased puts while accounting for the drag that buying them creates on the portfolio. In a future newsletter, we will make this calculator publicly available.

Again, the cash flow from step 3 makes this constant expense affordable.

5) Repeat or Sell Covered Calls

In the event that our puts expire worthless, we recycle the above process. In the event that we are exercised (meaning we must buy the shares), we will sell a covered call at or above our price point. This means that we are receiving premium up front in exchange for the promise to sell shares at a pre selected price. To account for some of the potentially missed upside, we will sometimes buy loose shares to capture some price appreciation.

It is worth nothing that even in this recent bull market, our strategy has not prohibited us from participating in the entirety of the market upside.

Additionally, in a steep decline, we can expect to be able to use proceeds from the long hedging put that we bought on the sector ETF to help lower our cost average to a point closer to which we can sell calls for profit.

While we try to leverage time decay by selling options closest to expiration, occasionally we will go further away from expiration if we must sell out of the money to generate maximum yield.

Strategy Summary

Even though we are still fine-tuning the particulars of our strategy, we believe that it stands to allow us to prioritize cash flow in such a way that will still increase total account value while also providing us with the consistent income needed to spend on counter bets. We hope that in the event of a crash, we will end up being in the position to pick through the ashes and increase our exposure to our favorite names at a discount.

Macroeconomic Trends

Generally speaking, the world economy (especially the US) has benefited from an influx of stimulus and the distribution of 3 vaccines that will help life return to normal; however, shifts during the now ending COVID period will more than likely have a fundamental effect on financial markets as a whole. As many do, we have an eye on rising interest rates. 3 major factors are outlined below:

Inflation

US Government Debt

Supplemental Leverage Ratios

Before you go on, we think it is important to note the differences between noise and a trend. For us, noise is an unsubstantiated attempt to explain market movements. A trend, on the other hand, is a substantial shift in a company, industry, or economy that we believe will have a significant fundamental impact on the markets or particular securities. Moreover, even though we believe that these trends will have a tangible impact on companies, we understand that not only can we not predict when these trends will affect price, but we cannot even really be certain that they will. There is always a chance that we were listening to noise rather than a trend. As a result, we try to pick stocks that we would be fine owning even if the impact of these trends was non-existent.

1) Inflation

The COVID-19 pandemic has unleashed the largest US government stimulus program in our country’s history. Over $5 Trillion has been deployed to help deal with the damage of the pandemic. Most of the money that is being used to fund these spending programs was originally borrowed by the US government, and much of that borrowed money came from the Federal Reserve printing trillions of dollars and loaning it to Uncle Sam.

Since March of 2020, the Federal Reserve has printed almost $5 trillion. This money has been loaned to the Federal Government and flows through small businesses via the Paycheck Protection Program, stimulus checks, and sometimes into the stock market. On the other hand, some of the money has landed in American’s savings accounts. Since March of last year, US citizens have saved more than an additional $3 trillion as a result of eating out less, fewer trips, and a surplus of cash from government transfers (stimulus checks).

Even with all of this money being printed, we’ve had almost no inflation.

Inflation is when more dollars or currency are chasing one product than there is supply for it. For example, concert tickets to a popular band: when these tickets go on sale, the amount of money chasing this product (ie, the number of people that want to buy these tickets) exceeds supply. The result is that prices controlled by the ticket seller and/or in the secondhand market will increase.

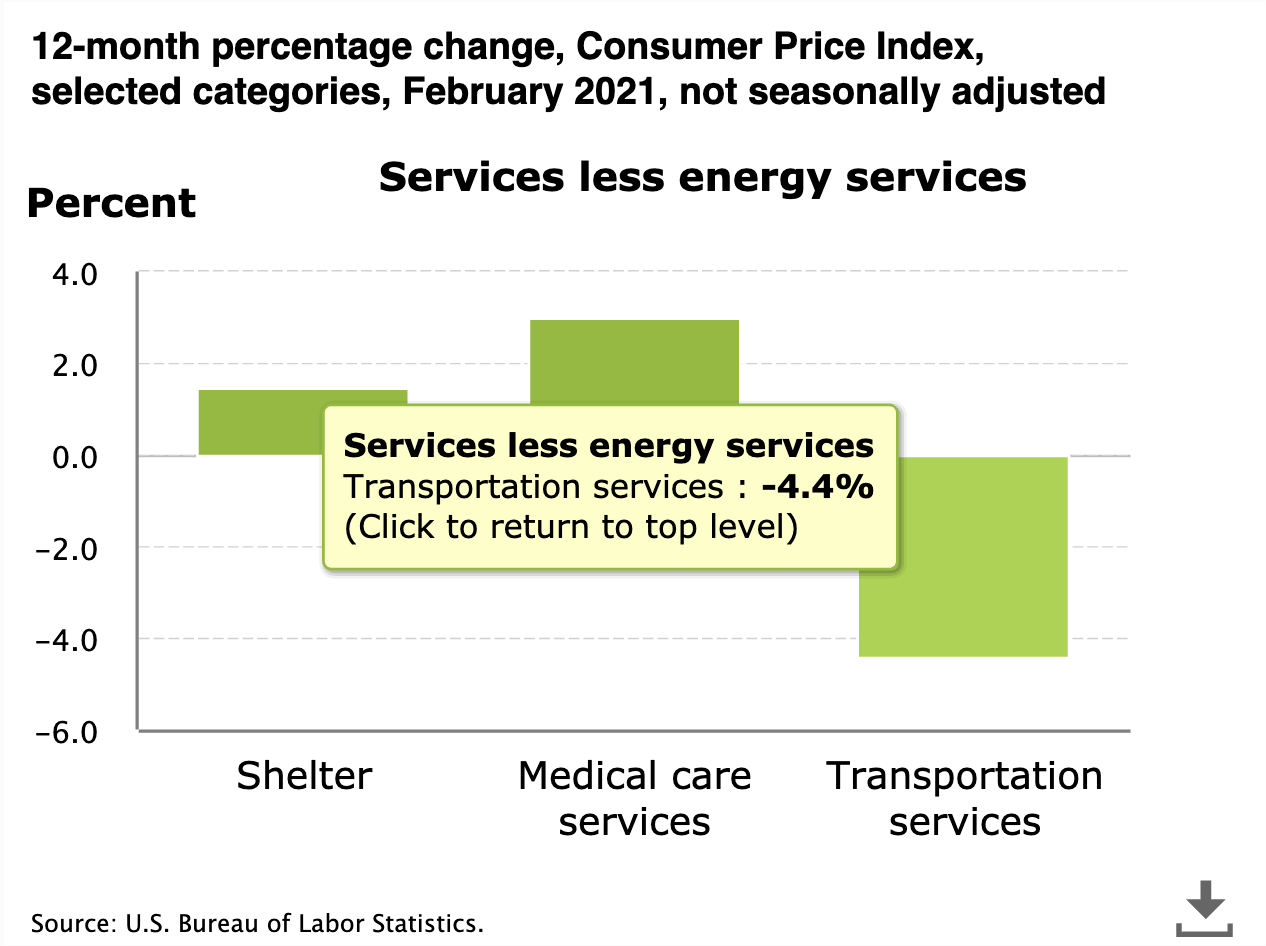

More important than understanding inflation is understanding how inflation is calculated. There are a few ways, but the one the Federal Reserve uses (and what we will reference) is similar to the CPI, or Consumer Price Index. This CPI is an index of commonly bought consumer goods in the US and is measured to show how inflation is performing. With this index, it measures an “average” inflation, meaning some prices can go up (food) and some can go down (airline tickets) resulting in net zero inflation. All this while the cost to buy a gallon of milk has gone up. This is without considering the Index’s rebalancing by the Bureau of Labor Statistics.

Going back to the present situation, inflation hasn’t happened yet because some goods, like airlines tickets and hotel bookings, aren’t being “chased” as some durable goods are, like home improvement supplies and new laptops for work at home. In other words, the prices for some goods have gone up and the prices for some goods have gone down. The result is that the headline numbers for inflation, the ones that decide interest rate decisions at the Federal Reserve, are not really budging (prices were only up 0.4% in the month of February).

Total prices seem tame (red) until you see some items are experiencing deflationary pressures (below)

So right now inflation is in check, right? Well, not exactly…

With consumers starting to get vaccinated, we expect them to spend more money in both categories - more money on durable goods such as new cars and appliances, and more on travel. This will cancel out the equalizing factors in the CPI and likely push prices up. Inflation is good to some degree, but some believe this could be some of the strongest inflation in a few decades.

Some of this has to do with the Velocity of Money.

The velocity of money is the speed at which the money flows through the economy. In fact, the size of the US economy is simply the quantity of money in circulation times the speed it's traveling. With the pandemic, the velocity dropped like a rock and the supply went up. They canceled each other out. But with the Federal Reserve continuing to print over $120 billion per month and the velocity soon accelerating, we see ample inflation inbound even if the velocity returned to just where it was pre pandemic.

The solution? Own names that benefit from rising inflation.

The easiest of these sectors are banks, especially those with high interest rate sensitivity. They make more money as they can charge more for loans, and with their depositors keeping more saved than ever, they have ample supply to lend. In fact, some banks are turning away deposits right now because they have no place to lend them. Banks will benefit from rising inflation, higher interest rates, and more income off their loans. Coincidentally, many banks also trade at attractive valuations. One of our favorites is Bank of New York Mellon. We’ve attached the research we used below; this is once again not investment advice, but we encourage you to read it for yourself.

2) US Government Debt

To go back to ECON 101 for all of us, we have to remember what causes interest rates to go up. For review, the costs to borrow go up or down essentially for two core reasons:

The expectation of inflation increases/decreases

The supply of loanable funds increases/decreases

We already discussed why we think inflation will go up and why this will increase interest rates, but we also have to discuss the equally important supply side. In essence, banks have a surplus of loanable funds right now that they don’t know where to park. But over the next few years two things may happen:

Consumers will spend much of these savings on demand for travel and other goods

The US government will need to borrow more money, and banks will buy more treasuries

Seeing as the second point is more debatable than the first, let’s focus on that. Since the great recession, millions of Americans have locked in low interest rates on their homes and other properties causing the money banks can make in this space to drop. Banks have instead loaned to corporations (where they can sometimes get variable interest rates) and simply held excess reserves. All of this, however, may change soon. The US government has run massive deficits over the past 12 months as the result of the pandemic. Fear, coupled with the Federal Reserve printing at over $120 billion a month, has led to most of the demand for US government debt to be satisfied as institutions, and investors have begun purchasing more treasuries. In fact, the US treasury actually had a cash balance of $1.6 trillion at the start of 2021, well over the $400-$500 billion that's normally required. But, with new stimulus and deficits well into the horizon, we’ll rapidly burn through this cash and have to borrow even more than we currently do on the open market.

How have current Treasury markets performed?

On this note, the current Treasury market is actually nearing a tipping point over the next few weeks. Back in February, the Treasury market had its worst appetite for US debt in 6 years. In other words, demand for treasuries at auction was the lowest in years. This caused yields to jump. What we are likely seeing is a major uptick in interest rates because the supply of loanable funds to the US government at these rock bottom interest rates are drying up. Once these bond yields go up, however, we could or could not see more demand from US banks (more on this later).

Doesn’t this solve the problem? Doesn’t the government then have ample money to borrow?

Not exactly. Like we mentioned, most of these ample reserves banks and consumers currently have could likely dry up as spending jumps and savings rates go down from their historical levels. This could accelerate the depletion of the supply of loanable funds, pushing US Treasury rates even higher. And if these rates move up, interest rates will too as many conventional debt products (mortgages, etc) base their rates on what the US 10 year bond is yielding.

In essence, interest rates now have 2 major reasons to jump.

3) Supplemental Leverage Ratios

The final trend we're watching is the Federal Reserve’s guidance on supplemental reserve ratios. The outcome of the final policy decision will decide how major US banks allocate capital to treasuries, how much in deposits they can hold, and even how much they will spend on dividends and buybacks. Let’s dive deeper.

The Supplemental Leverage Ratio (SLR) is the amount of money banks have in retained earnings or profits within the firm divided by the amount of other assets on the balance sheet. This could be customer deposits, treasuries, mortgages and more. The key reason this ratio exists is because firms need skin in the game so that if one of these assets go to 0, they can reimburse the losses with retained earnings, as most of these assets are bought with loans or with customer’s deposits. Currently, the SLR ratio is deemed to be 5% of assets. Now this is where it gets tricky!

Like we said before, the SLR is calculated by dividing retained earnings (the numerator) by assets (denominator). With the start of the pandemic, the government has issued huge amounts of treasuries and customer deposits have swelled as a result of COVID stimulus checks. With this, bank balance sheets have swelled to record numbers. However, due to loan loss reserves and falling profits, the retained earnings part of this equation has not kept up. In late March of 2020, many major US banks were close to the 5% SLR threshold. If they failed to stay above it, they would have had to halt dividends and share buybacks until the Federal Reserve gave their blessing.

Ouch!

So Chairmen Powell and the Federal Reserve reached a deal with the US banks in April of 2020: since US treasuries and new deposits are risk free assets (that is, the likelihood of them going to 0 is perceived to be impossible), you don’t have to keep incremental capital in the banks against these assets. In other words, you don’t have to collateralize these assets and they don’t have to count them in the denominator of the SLR ratio. This meant banks could reasonably continue to take customer deposits, loan money to the US government, and later resume share buybacks and dividends. All is good right?

Not exactly

In March of 2021, the Federal Reserve decided to end this waiver on the SLR for deposits and US treasuries. What this means is that banks will now have to keep cash as collateral against these assets. As a result, bank stocks have sold off as this could potentially mean less share buybacks, dividends, selling of treasuries and even refusing to take some deposits as hinted at this week by JP Morgan Chase. Below is a chart from Fitch Ratings detailing each major bank's SLR if the rules fully revert to normal at the end of this month. While no one would be under the 5% threshold, many banks may take preemptive measures to shore up their balance sheets by selling treasuries like we mentioned before. And, as we covered earlier in this newsletter, this is not ideal for the US treasury markets. The Federal Government is on pace to borrow more, not less, over the next 12 months than they have historically. The last thing they need is an excess of treasuries for sale. We believe this rule reversal will add to the pressure for higher interest rates in the United States over the next 6 months.

In summary, this could be a short-term pain for banks as they hold off on returning capital to shareholders.

It’s worth noting that smaller banks that are well above their SLR may benefit from these excess deposits coming in from larger banks that refuse them, and rising interest rates create more favorable loans. In the long run, however, rising interest rates are objectively good for institutions that make most of their net income off interest from loans. We see banks as potentially even more long term undervalued as a result of this rule change. The Federal Reserve has this policy change open for comment over the next few days, but places like Fitch do not believe that they will alter course. However, if they decide to keep some of these rules in place permanently, this could create a scenario where banks are still free to take more deposits while interest rates will continue to rise - so, even if the rule does not fall away, the banking sector could still benefit.

Summary

Overall, there are 3 large forces pushing up on interest rates - inflation, the government’s need for more money, and a shift in the SLR rules. While this is not necessary for a strong banking sector, it is undoubtedly a strong potential windfall, especially for the banks with the highest interest rate sensitivity.

Fund Performance

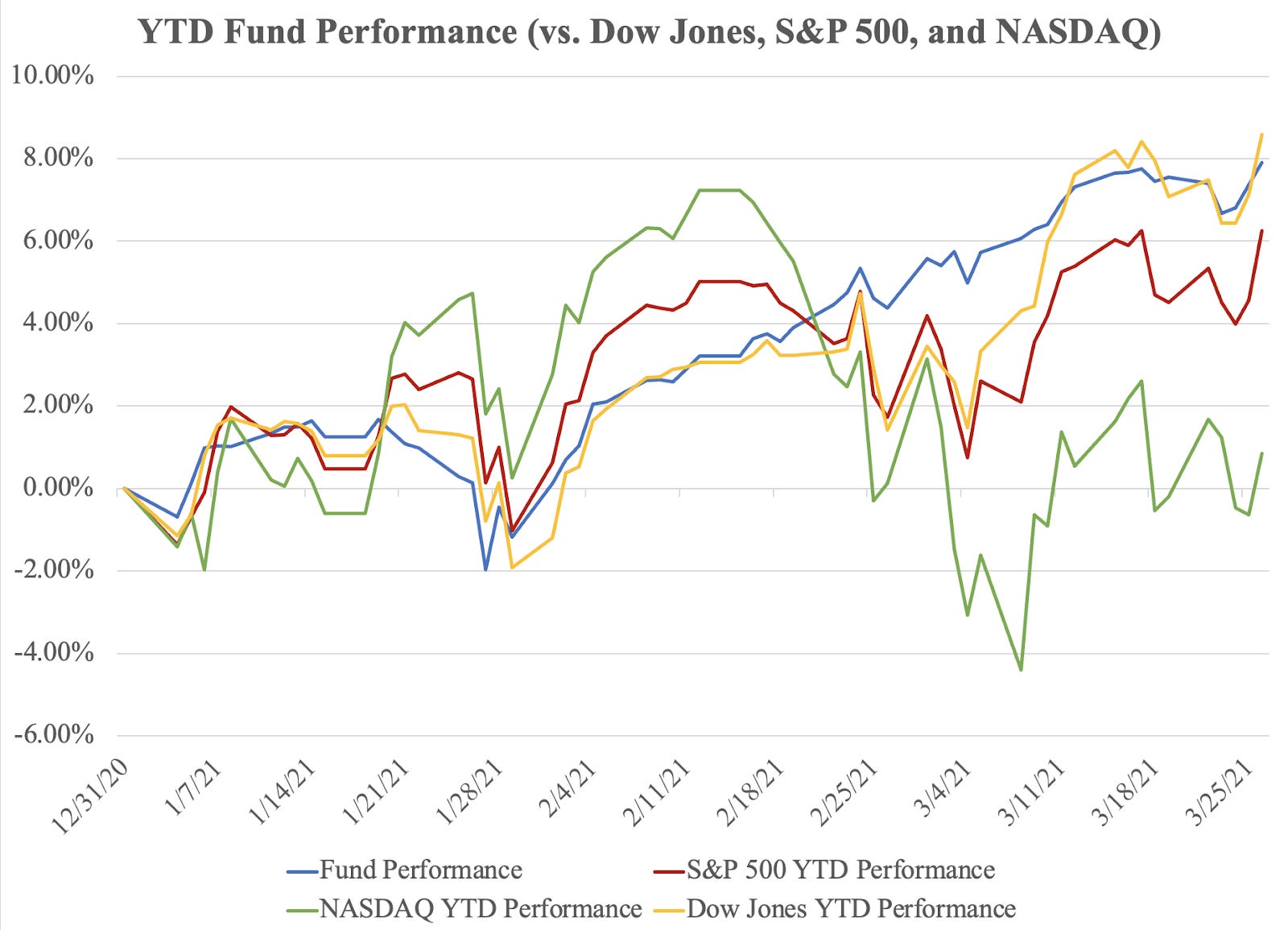

A few of our readers may already know we’ve put our money where our mouth is! Below is a summary of our fund’s performance since the start of 2021. While it looks good, it’s just an investment club brokerage account at TD Ameritrade we opened last year. Still, it’s putting us on track to hopefully take our first round of funding by the start of 2022.

That being said, it's important to realize that our goal isn’t necessarily to beat the S&P 500.

Why?

We’ve more or less tried to make our portfolio less risky than major indices; this claim, however, not only remains untested until a high impact event happens, but also does not give us an easy point of reference by which we can find an appropriate benchmark. Still, you may find it useful to see how we’ve been doing next to the major indices.

What’s Next?

We’ve attached a couple research reports for you to check out below. Although we’ve updated the numbers to represent price movements, the stocks now enjoy higher valuations and are, as a result, a little bit less attractive to us. To further emphasize this point, we are currently unrolling our positions to avoid a conflict of interest over the Summer. In the Fall, we will begin again in earnest with no intention of divesting in the near or long term.

You can expect a complete performance report in our next quarterly letter near the start of June. Some other topics on our minds for inclusion are the value of the Kelly Capital Growth Investment Criterion vs. the Capital Asset Pricing Model and a reexamination of the principles of the Intelligent Investor by Benjamin Graham in the era of cheap money… have value stocks finally made a comeback?

For now, we hope everyone enjoys the spring weather and sees some favorable returns!

Cheers,

Noah Cox - noahjcox9@gmail.com

Noah Jacobs - nkjczr@umich.edu